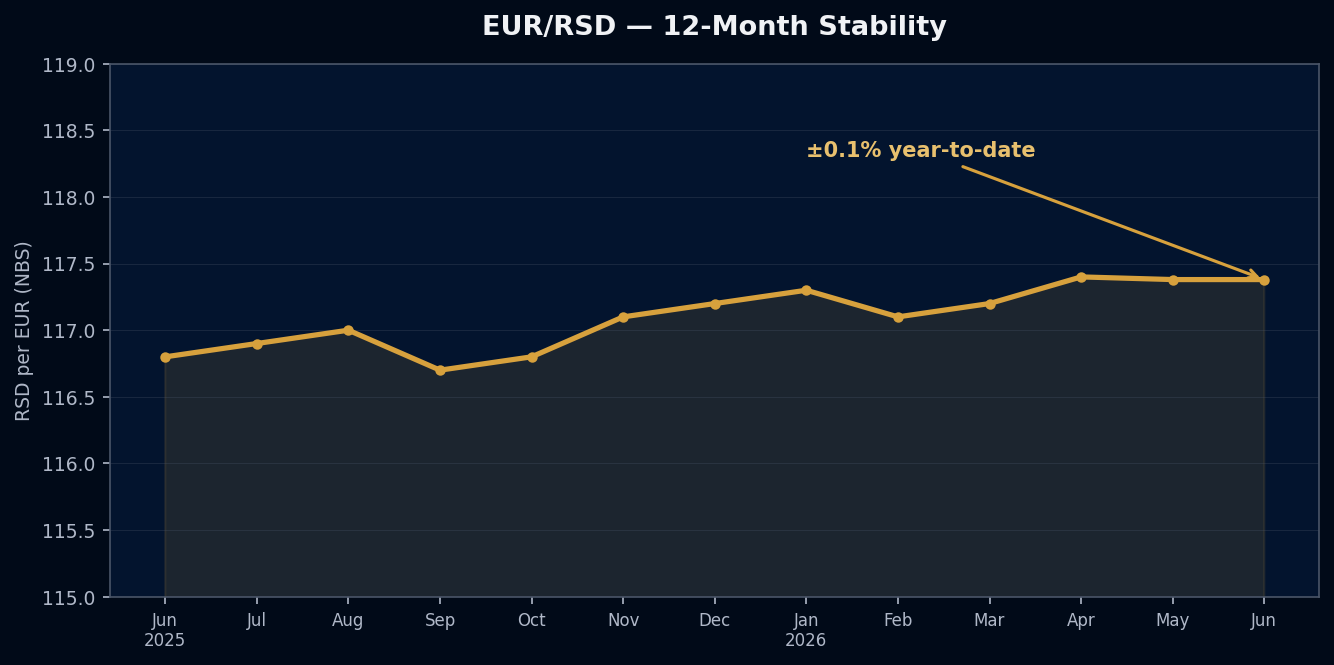

EUR/RSD is at 117.38 this week (NBS, June 2026). Twelve months ago, it was at approximately 117.0. The total move over the past year: less than half a percent.

For businesses operating in Serbia with EUR-denominated revenues — importers, distributors, service providers billing international clients — this stability is not an accident. It is a deliberate policy outcome maintained by the National Bank of Serbia through active FX interventions. Understanding what sustains it, and where the limits are, is relevant to any decision about dinar-denominated cost commitments.

How the NBS Holds the Corridor

Serbia operates a managed float for the dinar. Unlike fully fixed pegs (where the central bank commits to a specific rate) or fully free floats (where the market sets the rate), the NBS maintains a target corridor — typically within 1–2% of a reference rate — through regular open-market interventions.

The mechanism: when the dinar weakens toward the upper boundary of the corridor, the NBS sells EUR from reserves to buy dinars — supporting the rate. When it strengthens beyond the lower boundary, the reverse. The NBS has maintained substantial EUR reserves to support this operation, and the corridor has held through multiple external shocks over the past several years.

The practical result for businesses: your dinar-denominated costs — rent, salaries, local logistics, domestic suppliers — are not generating meaningful FX risk against EUR revenues this quarter. The rate you’re planning against today is, with high probability, the rate you’ll settle against next quarter.

What Stability in the Corridor Means for Importers

For a B2B importer with the following profile:

- Suppliers in Iran (costs ultimately tracked to IRR/USD)

- Operations in Serbia (costs in RSD)

- Customers in EU (revenues in EUR)

The EUR/RSD stability eliminates one of the three currency exposures entirely for operational planning purposes. The dinar-side cost base is, effectively, EUR-denominated — because the corridor guarantees the conversion.

This concentrates your actual FX risk entirely on the IRR side of the chain. The rial is moving at 112% annual depreciation while the dinar is moving at 0.1% annual change. The asymmetry between these two numbers is the core FX picture for EU–Iran–Serbia operations in 2026.

Practically, this means:

- Dinar-denominated costs can be included in EUR-basis financial models without a meaningful volatility assumption

- The risk budget for FX management should be allocated entirely to the IRR/USD monitoring function

- Long-term operational commitments in Serbia (facility leases, employment contracts) do not carry the currency risk premium they would in, for example, a Turkish lira or Egyptian pound environment

The Limits of Stability

Managed corridors are not permanent guarantees. The NBS has historically maintained this corridor well, but there are scenarios where pressure could exceed the bank’s intervention capacity:

External shock: A sudden deterioration in Serbia’s current account, a regional crisis that triggers capital outflows, or a significant EUR/USD move could pressure the NBS’s ability to defend the corridor at the current level.

Reserve depletion: Active intervention requires hard currency reserves. If the NBS needed to defend the corridor through an extended pressure period, reserve adequacy would matter. Serbia’s FX reserves are currently adequate, but this is a variable to monitor.

Political risk: Serbia’s EU accession process is ongoing. Any significant deterioration in the EU relationship could affect investor sentiment toward Serbian assets and, indirectly, dinar demand.

None of these scenarios are imminent in June 2026. But they are the conditions under which corridor stability would end — and any business building multi-year plans around dinar cost assumptions should have a contingency framing if the corridor widens.

The Practical Takeaway for This Quarter

For B2B operations with Serbia-based costs and EUR-denominated revenues, the current environment has two actionable implications:

1. Stop hedging dinar risk that isn’t there. Some businesses over-complicate their financial planning by adding a dinar volatility assumption that the data doesn’t support. At 0.1% movement year-to-date, dinar/EUR is not where your FX modelling effort should go.

2. Direct that effort toward the IRR side. The rial has moved 112%. That’s where margin compression is happening, where supplier repricing is building, and where quarterly monitoring pays off. A weekly 15-minute check of the TGJU rate tells you more about your actual cost exposure than any number of dinar/EUR sensitivity analyses.

The currency risk in EU–Iran–Serbia trade in 2026 is real — but it’s concentrated. Knowing where to focus is half the management problem.

Sources: EUR/RSD: National Bank of Serbia — nbs.rs | USD/IRR: TGJU — tgju.org/profile/price_dollar_rl

Follow the daily FX snapshot at t.me/ahooshai.