If you’re importing goods from Iran and selling to European buyers, you’re operating inside two currency systems that are moving in completely different directions.

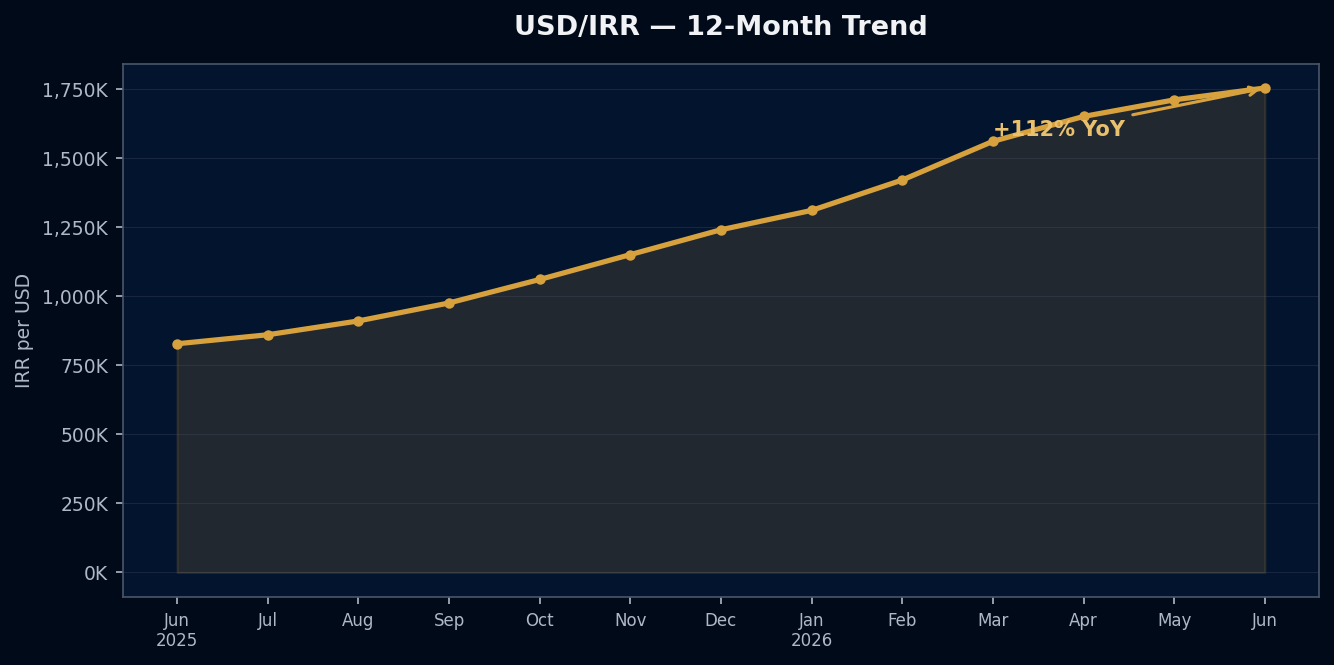

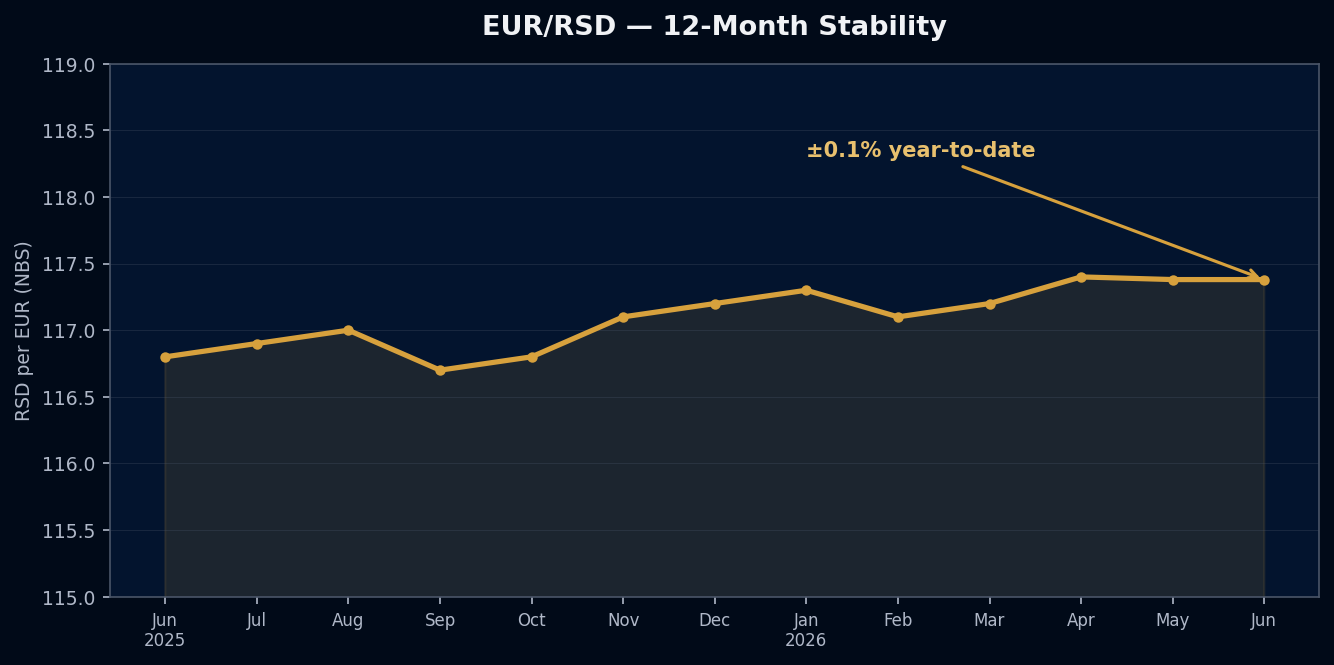

On one side: the Iranian rial, down 112% against the dollar over the past twelve months — from 827,400 to 1,753,000 IRR per USD (TGJU, June 2026). On the other: the Serbian dinar, stable within a ±0.1% corridor against the euro all year, held there deliberately by the National Bank of Serbia.

These two facts — one about cost-base compression, one about pricing stability — define the FX risk profile for EU-based importers working with Iranian suppliers in 2026. Understanding both is the starting point for any real risk management strategy.

The Two FX Exposures Every Importer Carries

Most B2B importers think of currency risk as a single number: “the exchange rate.” In practice, there are two separate exposures, and they move independently.

Exposure 1 — Your cost base. If your supplier is Iranian and quotes in IRR, your cost base is tied to the rial. When the rial weakens significantly, your cost per unit in EUR terms drops — unless your supplier adjusts prices upward to compensate. In a 112% depreciation environment, suppliers face enormous pressure to reprice. Some have. Many are still absorbing the gap between their IRR costs and their EUR-equivalent prices.

Exposure 2 — Your revenue base. If you’re selling to European buyers and invoicing in EUR, your revenue is EUR-denominated. The EUR/RSD corridor (117.38 as of June 2026, NBS) means your dinar-side costs — logistics, warehouse, local operations — are not generating currency risk this quarter. That’s a structural advantage specific to this moment.

The risk most importers miss is the interaction between these two exposures. If you’re invoicing your Iranian supplier in USD — as many trade routes default to — you’ve added a third currency into the chain, and you’re now exposed to EUR/USD movement on top of the IRR dynamics.

What the IRR Numbers Actually Mean

The 827,400 → 1,753,000 IRR/USD move happened across twelve months. That’s not a sudden crash — it’s a sustained, structural depreciation driven by sanctions pressure, domestic monetary policy, and capital controls that limit the central bank’s ability to defend the rate.

What this means for an importer:

Supplier cost bases have been crushed. A supplier paying 1,000,000 IRR per unit in raw materials in June 2025 is still paying roughly the same IRR amount — but in USD terms, that raw material cost has halved. This creates room for price renegotiation that didn’t exist twelve months ago.

Free-market rate vs. official rate diverges in crises. The TGJU figure (1,753,000) is the free-market rate. Iran’s Central Bank publishes a separate official rate that can differ by 30–50% in periods of political stress. If you’re using the official rate for your cost model, you’re working with the wrong number. The free-market rate is what your supplier’s actual procurement costs track.

The depreciation is not uniform across categories. Imported raw materials that Iranian suppliers buy in hard currency (USD/EUR) are fully exposed to the depreciation. Locally-sourced inputs — labor, domestic commodities — are not. Understanding your supplier’s input mix tells you how much of the 112% depreciation actually hits their cost structure.

EUR/RSD: The Stable Side of the Trade

While the rial has been in freefall, the dinar has been a non-event. EUR/RSD has moved less than 0.1% year-to-date, sitting at 117.38 (NBS, June 2026).

The NBS manages this stability through regular FX interventions — buying and selling dinars to keep the rate inside a narrow band against the euro. The corridor has held through multiple regional stress events. This quarter, there is no meaningful dinar-side FX risk for an EU-Serbia operation.

What this means practically: if your operating costs in Serbia are dinar-denominated and your revenues are EUR-denominated, you are not generating FX risk on that side of the ledger right now. The risk is entirely on the IRR/USD/EUR chain — and specifically, on how you structure the invoicing between yourself and your Iranian supplier.

The Three Structural Fixes

1. Invoice Iranian suppliers in EUR, not USD.

USD invoicing stacks IRR/USD risk on top of EUR/USD risk. Since your revenue is EUR and your Serbian costs are EUR-linked, EUR is the natural hedge currency for your cost base too. Many Iranian suppliers will accept EUR invoicing — especially when the EUR/USD rate is unfavorable for them in IRR conversion terms. It is worth asking directly.

2. Use TGJU free-market rates for all cost modelling.

Never use the Central Bank of Iran’s official rate for procurement cost calculations. The free-market rate (TGJU) is what suppliers’ actual procurement costs track, and it’s what matters for any renegotiation conversation. This is the rate at: tgju.org/profile/price_dollar_rl.

3. Build in a weekly review cadence during high-volatility periods.

The IRR depreciation has not been linear — there have been acceleration phases (typically around political events) and plateau phases. A weekly rate review — 15 minutes, pulling TGJU and NBS figures — catches inflection points before they turn into unpriced cost surprises. Monthly reviews in this environment miss too much.

The Risk You Don’t See

The subtler risk in the EU–Iran import corridor in 2026 is not the rate move itself — it’s the asymmetry in who absorbs it. When the rial weakens fast, Iranian suppliers often absorb the cost gap silently for one or two quarters, then reprice sharply to catch up. The importer who hasn’t been tracking the rate has no warning when the repricing comes — it looks like a supplier decision, not a currency event.

Building the rate into your quarterly supplier reviews — as a shared data point, not a negotiation weapon — makes the repricing conversation predictable for both sides.

AHoosh works with B2B importers to build FX risk frameworks that connect currency data to actual procurement decisions. If you want to review your current exposure structure, reach us at ahoosh.ai/contact.

Daily FX briefings at t.me/ahooshai.