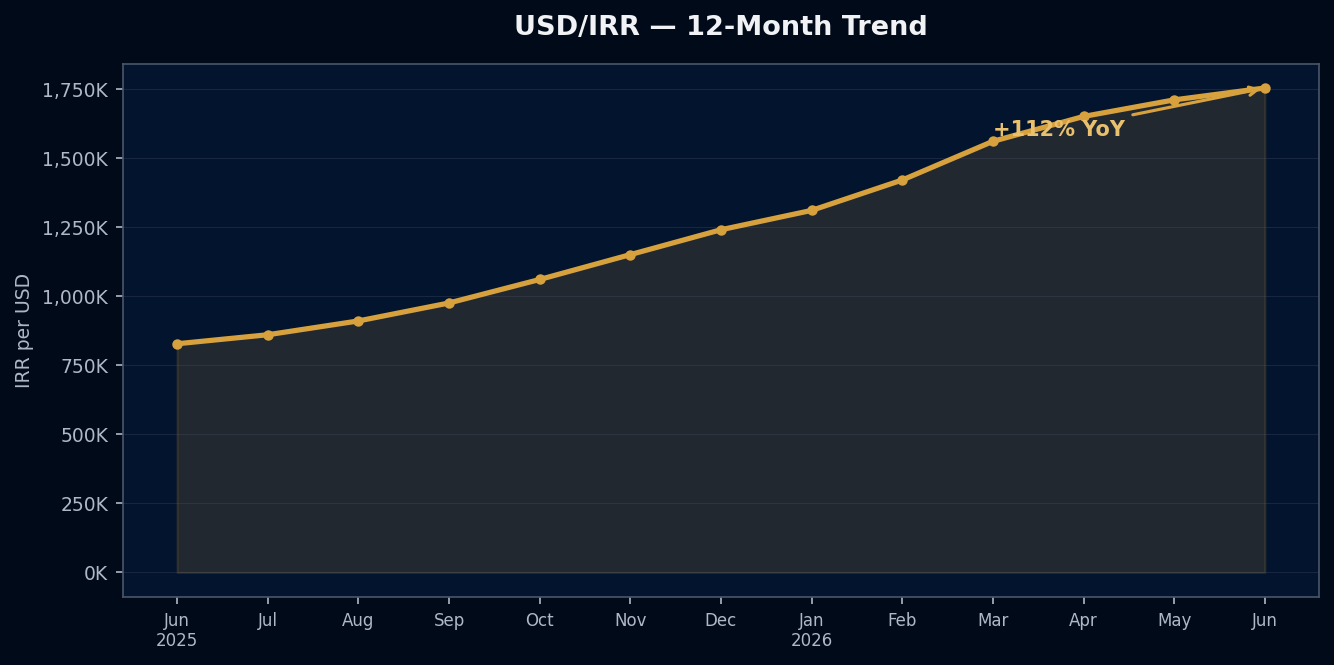

The Iranian rial lost 112% of its value against the US dollar over the past twelve months. That’s the headline number — 827,400 to 1,753,000 IRR per USD, tracked on the free-market rate (TGJU).

But the headline number is not the supply chain number. What matters for an importer is not the rate itself — it’s what the rate does to your supplier’s cost structure, their pricing floor, and the renegotiation leverage it creates or destroys.

How Depreciation Transmits Into Supplier Pricing

Iranian manufacturers and distributors operate with a mixed cost base. Some inputs are imported and priced in hard currency (USD or EUR). Some are domestic — labor, locally-sourced materials, domestic energy. The depreciation affects these categories differently.

Hard-currency inputs: Any raw material or component that the supplier imports is now roughly twice as expensive in IRR terms as it was twelve months ago. The supplier who was paying 1,000,000 IRR for a component is now paying ~2,100,000 IRR for the same component — if the component is USD-priced and they’re buying at the free-market rate.

Domestic inputs: Labor, local materials, and domestically-produced components are not directly indexed to the USD rate. They inflate at a different pace — typically tied to domestic inflation, which runs high in Iran but is not a 1:1 mirror of the exchange rate move.

The net effect: Suppliers with high import content in their cost base have been squeezed badly. Their costs have roughly doubled in IRR terms on the hard-currency side, while their EUR-denominated export prices may not have moved proportionally. This compression is the negotiation lever.

The Compression Window

Here’s the paradox the depreciation creates for EU importers: a weaker rial, counterintuitively, can improve your cost position — if you act on it.

When the rial weakens faster than Iranian suppliers can reprice to European buyers, the EUR-equivalent cost of Iranian goods drops. The supplier’s IRR revenue stays roughly stable in their domestic accounting. But in EUR terms, they’re receiving less per unit than before.

This compression window — the gap between the rate move and the repricing response — is typically 3–6 months. Suppliers operating with annual or semi-annual price reviews are often sitting inside this window right now: their IRR-denominated costs have risen, but their EUR quotes to European buyers haven’t fully caught up.

The importer who recognizes this and opens a renegotiation conversation before the supplier initiates one is in a structurally better position. The supplier is under margin pressure. A volume commitment or longer contract term in exchange for a better EUR unit price can work for both sides.

What ‘Free-Market Rate’ Actually Means in Practice

There are two USD/IRR rates that exist simultaneously in Iran:

The Central Bank rate (NIMA): The official rate, used for certain government transactions and heavily subsidized imports. This rate is managed and typically 30–50% stronger than the free-market rate in stress periods. If your supplier gives you a price and says “based on the official rate” — that price does not reflect their real procurement costs.

The free-market rate (TGJU): The rate at which Iranian businesses actually buy and sell hard currency for commercial transactions. This is the rate that tracks to your supplier’s real cost base. It’s publicly available at tgju.org/profile/price_dollar_rl and is updated in real time.

For any cost modelling, use the TGJU rate. For any pricing conversation with a supplier, confirm which rate they’re using. The difference between the two rates can make a quoted EUR price look better than the supplier’s actual economics support — which means a repricing surprise later.

Three Practical Responses

1. Audit your supplier’s cost structure before the next renewal.

Ask your key suppliers to walk you through their input mix: what percentage of their raw materials are imported, and at what rate do they buy hard currency? This conversation is not unusual — it’s the foundation of a responsible procurement relationship. The answer tells you how exposed they are to the depreciation and how much room exists in their pricing.

2. Lock longer contracts while compression exists.

If your supplier’s EUR-denominated prices have not yet adjusted to the full extent of the depreciation, a 12–18 month fixed-price contract (with a reasonable escalation clause) protects you against the inevitable repricing catch-up. Suppliers under margin pressure often prefer the volume certainty of a longer contract over the flexibility of quarterly repricing.

3. Benchmark against multiple suppliers.

The 112% depreciation has not hit all suppliers equally. A supplier with high domestic input content and strong local sales will have absorbed the depreciation better than one fully exposed to USD-priced imports. Running a quiet benchmarking exercise — even without intent to switch — gives you market data for the pricing conversation.

The Risk Going Forward

The structural drivers of IRR depreciation — sanctions pressure, domestic monetary policy, capital controls — have not changed in 2026. The rate could stabilize at current levels or continue weakening. It is not likely to reverse significantly in the near term.

For supply chain planning purposes, this means:

- Do not build long-term cost models using the current IRR rate as a floor

- Build in a quarterly rate review and a price adjustment mechanism in supplier contracts

- For any supplier relationship you intend to maintain for 2+ years, the currency conversation is part of the commercial relationship, not a negotiation tactic

The importers who treat IRR volatility as a known operational variable — and build it into procurement workflows — end up with fewer surprises and better supplier relationships than the ones who ignore it until a price increase arrives.

AHoosh helps B2B importers build procurement frameworks that account for currency volatility in emerging market supply chains. Contact: ahoosh.ai/contact — or follow the daily FX briefing at t.me/ahooshai.