The first time a small consultancy or agency invoices a client in another EU country, the VAT question usually causes a small panic. Do I charge my local VAT rate? Their rate? No VAT at all? Get it wrong and you either overcharge a client who queries it, or undercharge and end up owing tax you never collected. Neither is fatal, but both waste time and erode the professional impression you are trying to make.

The good news is that for B2B services between EU countries, the rules are more consistent than they look, and most cross-border service invoices follow one mechanism: the reverse charge. Once you understand that mechanism and the handful of checks around it, cross-border invoicing becomes routine. The bad news is that “it depends” is a real answer for edge cases, and a few specifics genuinely require a local accountant.

This guide covers the practical path for a small B2B service firm invoicing across EU borders: how the reverse charge works, the checks you must do before applying it, what a compliant invoice needs, and the mistakes that cause problems later. It is orientation, not tax advice — treat a qualified accountant as the final word on your situation.

The Reverse Charge — The Default for B2B EU Services

For most B2B services between EU countries, you do not charge VAT.

Under the EU’s place-of-supply rules, most business-to-business services are taxed where the customer is established, not where the supplier is. In practice, when you (an EU business) supply a service to a business customer in another EU country, you generally issue the invoice without VAT, and the customer accounts for the VAT in their own country under the “reverse charge.” They both charge and reclaim it in their return, so it usually nets to zero for them — but the obligation sits with them, not you.

What this means on your invoice:

- You charge €0 VAT on the service

- You state the net amount only

- You add a note indicating the reverse charge applies (wording below)

- The customer self-accounts for VAT at their local rate

Why the mechanism exists.

The reverse charge shifts the VAT accounting to the customer’s country so that cross-border trade is not distorted by suppliers charging their home rate to foreign businesses. It keeps VAT neutral for legitimate B2B trade and reduces the need for suppliers to register for VAT in every country they sell into. The European Commission’s VAT rules for services set the framework; national implementations follow it.

The general B2B rule has exceptions.

Some services are taxed differently — services connected to immovable property (taxed where the property is), certain events, restaurant and transport services, and a few others follow special place-of-supply rules. If your service touches one of these categories, the general reverse charge may not apply and you should check the specific rule. For standard professional services — consulting, design, software, marketing — the general B2B rule usually holds.

Before You Apply the Reverse Charge — The Checks You Must Do

Verify the customer is a business with a valid VAT number.

The reverse charge only applies to genuine B2B supplies where the customer is a taxable person in another EU country. You cannot just take their word for it — you need their VAT identification number and you should verify it.

Use VIES to check the VAT number.

The EU runs VIES, a free tool that confirms whether a VAT number is valid and active in another member state. Before applying the reverse charge:

- Get the customer’s full VAT number including country prefix

- Check it in VIES and confirm it is valid

- Keep a record of the check (date, result) — if a tax authority later questions the invoice, evidence you verified matters

If the customer has no valid VAT number.

If they cannot provide a valid VAT number, they may not qualify as a business for these purposes, and you might have to treat the supply differently — potentially charging your local VAT. This is a common trap: applying the reverse charge to a customer who turns out not to be VAT-registered can leave you owing the tax. When in doubt, verify first and ask your accountant about the specific case.

B2C is a different world.

If your customer is a private consumer rather than a business, entirely different rules apply — often you charge VAT, and for certain digital services the OSS (One Stop Shop) scheme comes into play. This guide is about B2B; the moment you sell to consumers cross-border, get specific advice, because the thresholds and registration duties change.

What a Compliant Cross-Border Invoice Needs

Standard required elements.

Whatever the VAT treatment, an EU invoice generally needs a consistent set of details. Missing elements can cause a client’s accountant to reject it and delay payment:

- A unique sequential invoice number

- Invoice date (and date of supply if different)

- Your full business name, address, and VAT number

- The customer’s full business name, address, and VAT number

- A clear description of the services supplied

- The net amount and currency

- The VAT rate applied (here, 0 / reverse charge) and VAT amount

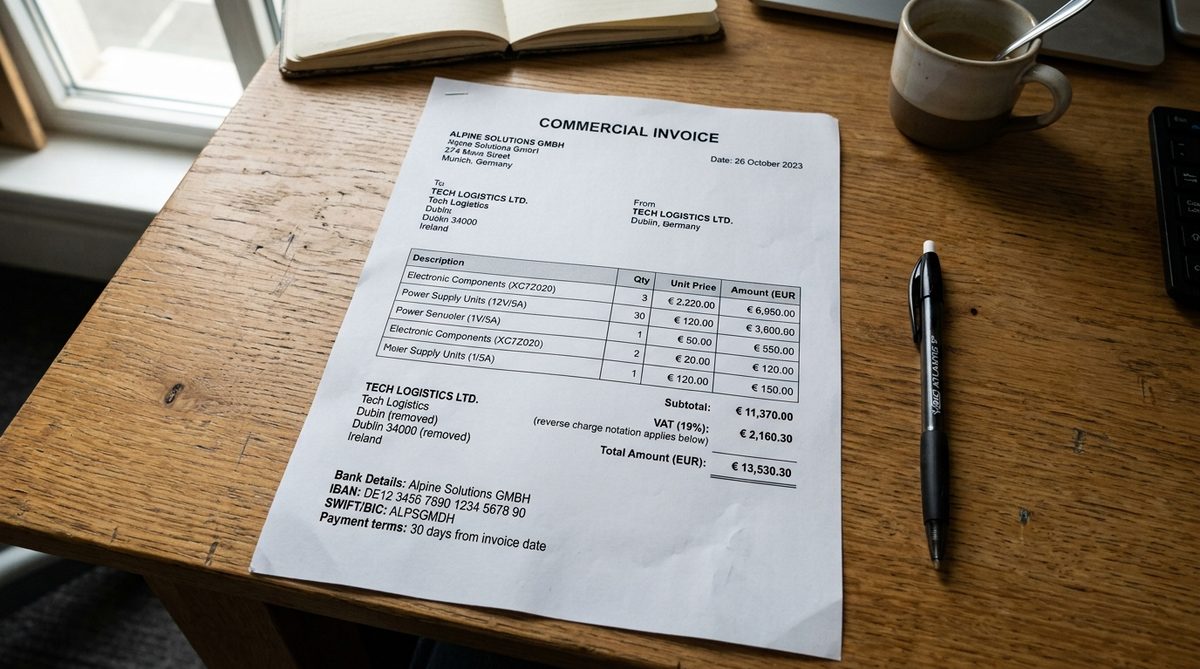

The reverse-charge wording.

For a reverse-charge invoice, add an explicit note. A widely accepted form is: “Reverse charge — VAT to be accounted for by the recipient.” Stating the mechanism plainly tells the customer’s accountant exactly how to treat it and shows the tax authority you applied the rule knowingly. Include the customer’s verified VAT number on the invoice as part of the evidence.

Currency and language.

- You can invoice in euros or another currency by agreement; if you invoice in a foreign currency, keep clear records of the exchange rate used for your own VAT reporting

- Invoicing in the client’s language or bilingually smooths payment, though it is a courtesy, not a legal must

- Currency swings on cross-border invoices are a real cost — the mechanics of managing that exposure are covered in FX risk for B2B importers

Report it correctly on your side.

Cross-border B2B services usually go on an EC Sales List (recapitulative statement) in addition to your normal VAT return, declaring the value supplied to each customer’s VAT number. Your accounting software or accountant handles this, but know it exists — it is how tax authorities cross-check that the customer actually accounted for the reverse charge.

Common Mistakes and How to Avoid Them

Charging your home VAT to an EU business customer.

The most frequent error: adding your local VAT rate to a B2B invoice that should have been zero-rated under the reverse charge. The client’s accountant queries it, you reissue, and you look like you do not know the rules. Confirm the reverse charge applies before you add any VAT.

Applying the reverse charge without verifying the VAT number.

The mirror mistake: zero-rating an invoice for a “business” that turns out not to be validly VAT-registered, leaving you liable for the tax. Always run the VIES check and keep the record. Verification is a two-minute step that prevents a genuine liability.

Assuming e-invoicing rules are uniform.

Several EU countries are rolling out mandatory structured e-invoicing (machine-readable formats, sometimes routed through government platforms) on staggered timelines through the mid-2020s. If you invoice into a country moving to mandatory e-invoicing, a PDF may not satisfy the rules. Check the current requirement for the countries you sell into, because this is changing quickly.

Forgetting the paperwork trail.

VAT is an evidence game. Keep VIES check records, copies of every invoice, exchange rates used, and your EC Sales List filings. If a tax authority ever reviews a cross-border supply, the difference between a quick clearance and a painful audit is whether you can show the checks you did. A tidy, consistent process — the same discipline behind Incoterms and documentation for B2B trade — pays off precisely when it is questioned.

Treating “it depends” as an excuse to guess.

Special-category services, B2C supplies, and non-EU customers all follow different rules. When your situation is outside the standard B2B EU service, that is the signal to ask an accountant, not to improvise. The cost of a short consultation is trivial against the cost of a systematic error repeated across a year of invoices.

For the everyday case — a small EU service firm invoicing a business customer in another EU country for consulting, design, software, or marketing — the path is clean: verify the customer’s VAT number in VIES, issue the invoice with no VAT under the reverse charge, add the correct wording and the customer’s VAT number, and report it on your EC Sales List. Do that consistently and cross-border invoicing stops being stressful.

Keep the evidence, watch the country-specific e-invoicing changes, and reserve your accountant’s time for the genuine edge cases — property-linked services, consumer sales, and non-EU customers. The routine is routine once you have done it a few times; the discipline is in the checks, not the calculation.

Sources: European Commission — VAT rules and directive · European Commission — VIES VAT number validation